“The main reason people struggle financially is because they have spent years in school but learned nothing about money. The result is that people learn to work for money… but never learn to have money work for them.”

– Robert T. Kiyosaki, Rich Dad Poor Dad

Introduction

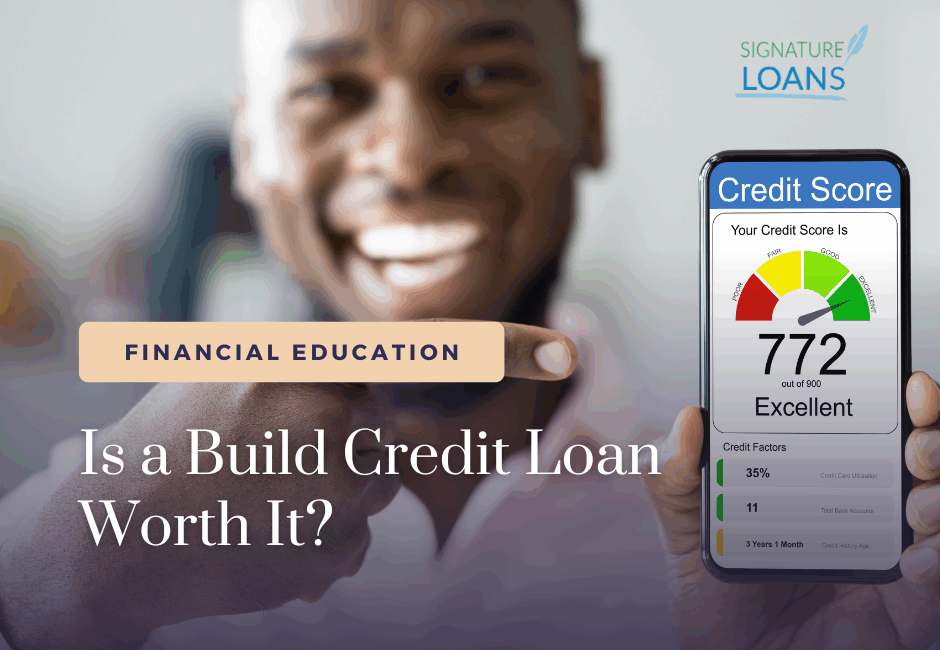

When you have no credit history or your credit score is poor, it can feel like you’re locked out of the financial system.

Traditional lenders rely on credit scores to decide whether you’re a trustworthy borrower, which makes it hard to prove yourself if you’ve never had credit.

Build credit loans, also called credit‑builder loans are designed for this exact situation.

In this guide, we’ll explore what these loans are, how they work, who should consider them, and whether they’re truly worth it.

Everything You Need to Know About Build Credit Loans

1 What Is a Build Credit Loan and How Does It Work?

A build credit loan is an installment loan specifically created to help people establish or repair a credit history.

A build credit loan is an installment loan specifically created to help people establish or repair a credit history.

Instead of receiving a lump sum at the outset, you make monthly payments toward a loan amount that the lender holds in a secured account—often a savings account or certificate of deposit (CD).

Once you’ve repaid the loan, the lender releases the funds to you, minus any interest and fees.

Because the lender reports your payments to major credit bureaus, consistent on‑time payments can build or improve your credit score.

This “pay first, receive later” structure is very different from typical personal loans, which give you money up front.

Step‑by‑Step Process

-

- Apply and get approved. Build credit loans generally don’t require a strong credit history. Some lenders may not perform a hard credit inquiry at all, but you’ll need to show stable income and be at least 18 years old. For example, lenders like Self require a bank account or debit card to qualify.

-

- Funds are held in a secured account. Instead of giving you cash, the lender deposits the loan amount (typically $300–$1,000) into a savings account or CD.

-

- Make monthly payments. You make fixed payments over six to 24 months. Payments often start as low as $10–$25 per month, though the exact amount depends on the lender and loan size. Lenders report these payments to the three major credit bureaus—Equifax, Experian and TransUnion.

-

- Receive funds at the end of the term. After repaying the loan, you receive the money you’ve been paying into the secured account, minus any fees or interest charges.

This structure benefits lenders because they have security in the form of your payments. It benefits borrowers by creating a positive payment history, which is one of the most significant factors in a credit score.

2 Why Do Build Credit Loans Help Your Credit Score?

Credit scores are calculated using several factors, and payment history carries the most weight.

Making on‑time payments toward a build credit loan shows future lenders that you’re reliable, and this can increase your score over time.

Additionally, taking on a build credit loan adds variety to your credit mix; credit bureaus like to see a combination of installment loans (like auto loans, mortgages or credit‑builder loans) and revolving credit (like credit cards).

A more diverse credit mix contributes about 10% of your score and can improve it if you have limited history. However, missing payments harms your credit.

Lenders typically report payments that are 30 days late or more to the credit bureaus, and these negative marks can remain on your report for seven years. That’s why it’s crucial to choose a loan amount and monthly payment that fits your budget and to set up automatic payments if possible.

3 Who Should Consider a Build Credit Loan?

Build credit loans are best suited for individuals who:

-

- Have no credit history or limited credit. Young adults or recent immigrants who haven’t used credit before can benefit from establishing a credit record.

-

- Have poor or fair credit and need to rebuild. If your credit score suffered due to past issues but you’re now in a position to make consistent payments, a credit‑builder loan may help you regain lenders’ trust.

-

- Can afford small monthly payments and don’t need immediate cash. These loans hold your funds until the term ends, so they’re not ideal if you need money right away.

The Consumer Financial Protection Bureau (CFPB) found that credit‑builder loans are most effective for borrowers without existing debt; those without debt experienced credit score increases roughly 60 points higher than those with debt.

If you already have multiple debt obligations, a build credit loan may not deliver the same benefit and could make repayment more challenging.

4 Pros and Cons of Build Credit Loans

Pros

-

- Accessible to credit newcomers. Many lenders don’t require good credit for approval.

-

- Helps establish payment history and diversify credit mix. On‑time payments contribute to your score and show you can manage installment debt.

-

- Forces savings. Because the funds are locked in a secure account until you finish repayment, you end up with a small nest egg or emergency fund at the end.

-

- No large up‑front deposit. You don’t need to deposit the entire loan amount up front (unlike secured credit cards), making it easier for borrowers with limited cash.

Cons

-

- Delayed access to funds. You won’t get the money until the loan is paid off.

-

- Interest and fees apply. Build credit loans aren’t free. You’ll pay interest, and some lenders charge administrative fees or late fees.

-

- Potential harm if mismanaged. Missing payments can hurt your credit score more than the loan helps.

-

- Limited loan amounts. These loans typically range between a few hundred and a few thousand dollars. They’re not suited for large purchases.

Evaluating these pros and cons will help you decide whether the benefits outweigh the drawbacks.

5 How Do Build Credit Loans Compare With Secured Credit Cards?

Another common way to build or rebuild credit is by using a secured credit card. You deposit a set amount, often $200–$500 and the card’s credit limit equals or is tied to your deposit.

Each month you charge and pay off purchases, and the issuer reports your activity to the bureaus. Here’s how secured cards and build credit loans stack up:

| Feature | Build Credit Loan | Secured Credit Card |

|---|---|---|

| Collateral | Funds withheld until loan is repaid | Cash deposit held as collateral |

| Up‑front cost | No large deposit; you make monthly payments | Deposit required before use |

| Credit type | Installment credit | Revolving credit |

| Payment structure | Fixed monthly payments for 6–24 months | Flexible payments; you choose how much to pay above the minimum |

| Access to funds | Funds released after loan term | Access to revolving line of credit immediately |

| Who it’s best for | People without savings for a deposit or those who want a forced savings plan | People who have a deposit and want to build credit through regular card use |

Both products can be effective if used responsibly.

Credit scores benefit from having both installment and revolving accounts, so some borrowers choose to use a secured card and a credit‑builder loan simultaneously.

6 How to Choose the Right Build Credit Loan

Not all credit‑builder loans are alike. Before applying, consider the following factors:

Not all credit‑builder loans are alike. Before applying, consider the following factors:

-

- Annual percentage rate (APR). Loan APRs often range from around 10% to 15%, though they can be higher. Compare rates across lenders and watch for additional fees.

-

- Loan size and term. Choose a loan amount and monthly payment you can comfortably afford. Shorter terms cost less in interest but require larger payments.

-

- Reporting to all three bureaus. Confirm that the lender reports to Equifax, Experian and TransUnion. Otherwise, your positive payment history might not be recorded across the board.

-

- Loan origination and late fees. Ask about any setup or account fees that could reduce the amount you receive at the end. Also, check the lender’s policy on late payments; some charge up to 5% if you’re over 15 days late.

-

- Customer service and educational tools. Lenders such as Self and other online platforms often include credit monitoring and educational resources.

We recommend making a shortlist of potential lenders, including local credit unions, community banks, and reputable online providers. Compare their terms side by side. Choose the option with transparent fees, reasonable rates, and strong customer reviews.

7 Alternatives to Build Credit Loans

If you decide a build credit loan isn’t right for you, there are other ways to establish or improve your credit:

-

- Become an authorized user. Ask a trusted family member or friend with a good credit history to add you as an authorized user on their credit card. You won’t need to use the card to benefit from their positive payment history.

-

- Get a co‑signed loan or credit card. Applying with a co‑signer may help you qualify for traditional credit products, but both parties are legally responsible for the debt.

-

- Secure a credit card. A secured credit card is a good alternative if you have a deposit and want access to credit immediately.

-

- Use rent or bill reporting services. Some services report rent or utility payments to credit bureaus, helping you build a payment history without borrowing.

Each method has its own pros and cons, so think about your financial situation and choose the strategy that aligns with your needs.

8 Conclusion – Is a Build Credit Loan Worth It?

So, is a build credit loan worth it? It depends on your circumstances.

If you don’t have a credit history or your credit score is too low to qualify for traditional loans or credit cards, a build credit loan can be a valuable tool for establishing positive payment history. These loans are generally easy to qualify for, don’t require large up‑front deposits, and encourage saving.

For borrowers who can commit to small, on‑time payments and don’t need immediate access to funds, the benefits often outweigh the costs.

However, build credit loans aren’t a magic solution. They come with interest and fees, and the amounts are too small for large purchases.

If you already carry debt, adding another monthly payment could strain your budget and hurt rather than help your credit. And if you miss payments, you risk damaging your score and losing the benefit of the loan.

In summary, a build credit loan is worth it for people who need to establish or rebuild credit and can handle consistent payments. But it’s not ideal for those needing cash immediately or those who cannot afford the additional monthly obligation.

We encourage readers to evaluate their financial circumstances, compare lenders, and consider alternative credit‑building options before applying.

9 What are credit building loans?

Credit building loans are small loans designed to help you establish or rebuild credit by making monthly payments that get reported to the credit bureaus.

10 How do credit builder loans work?

You make fixed monthly payments while the lender holds the loan amount in a secured account. After you finish paying, you get the money back (minus fees).

11 Are credit builder loans worth it?

Yes, if you follow the payment schedule. They are one of the safest and most predictable ways to build a positive payment history.

12 Should I get a loan to build credit?

If you have no credit or damaged credit, a credit builder loan is one of the simplest and lowest-risk places to start.

13 Are credit builder loans good?

They’re good for people with poor or no credit who want a structured, safe way to build a payment history.

14 My credit is terrible… is a Build Credit Loan actually going to help me or am I wasting my time?

If you make every payment on time, a Build Credit Loan can absolutely help rebuild your score; this is exactly what they’re designed for.

15 I’ve never built credit before. What’s the easiest legit way to start from zero?

A credit builder loan is one of the easiest ways to get started because you don’t need established credit to qualify.

16 Is there a safe way to build credit without getting into debt?

Yes, a credit builder loan is safe because the funds are held for you, and you’re building credit while essentially saving money.

17 I can’t get approved anywhere. Would a Build Credit Loan help me qualify for real loans later?

Yes. Consistent on-time payments help you build enough credit history to qualify for personal loans, auto loans, and even apartments later.

18 Does a credit builder really work for someone with no credit or only for people rebuilding?

It works for both. It helps the credit-invisible start fresh and also helps rebuilders create new positive payment history.

19 How long does it take before a Build Credit Loan actually improves my score?

Many people see improvement in 2–6 months with perfect on-time payments, though results vary.

20 Where do people with bad credit actually start building credit without getting scammed?

A legitimate credit builder loan is one of the safest options because it’s regulated and reports directly to the three credit bureaus.

21 I already have fair/good credit… can I use a personal loan to wipe out my other debts fast?

Yes, a signature loan can be used as a debt consolidation loan to combine your balances into one predictable monthly payment.

22 I don’t need to build credit. I need a single loan to pay everything off. What’s the best option?

A signature loan is typically the best choice if your credit is already strong and you need funds now.

23 Can I get approved for a debt consolidation loan today if I have stable income?

If your credit is fair or good, many lenders approve same-day decisions for signature loans.

24 I have a job but bad credit. Where can I get a quick loan without getting denied again?

A payday loan is often the simplest option for borrowers with steady income and low credit scores.

25 Can I get a small loan before payday even if my credit score is low?

Yes, payday loans are designed for quick approval based on your job, not your credit score.

26 How do I know if I should build credit or consolidate debt instead?

If you need money now, consider consolidating. If your main goal is improving your score, start with a credit builder.

27 How do I choose between building credit slowly or applying for a loan today?

If timing is urgent, apply for a loan. If your priority is long-term credit health, a builder loan is safer.

28 I’m tired of getting denied for apartments and car loans. Will a credit builder fix this?

Yes, building a stronger credit history through consistent on-time payments improves your approval chances for apartments, auto loans, and more.

Ready to Fix Your Credit or Consolidate Your Debt Today?

If you’re serious about building or rebuilding your credit, the fastest place to begin is right here. Tap this link to start your journey with a trusted credit-building partner:

👉 https://www.self.inc

But if you don’t want to use a credit builder program, you still have strong options.

Right below, you’ll find two fast and simple loan applications. Choose what fits your situation:

- Signature Loan (Debt Consolidation Option): Ideal if you already have a solid credit history and want to consolidate high-interest debt or get a personal loan today.

- Payday Loan: A quick option for borrowers who have a steady job but less-than-perfect credit and need fast cash now.

Choose the path that supports your financial goals. Everything you need is right below.

Apply for a Personal Signature Loan

+ Apply for a Payday Loan (Click to Open)

The information above is provided for general educational purposes. Always review the terms and conditions of any loan and consult a financial advisor if needed.